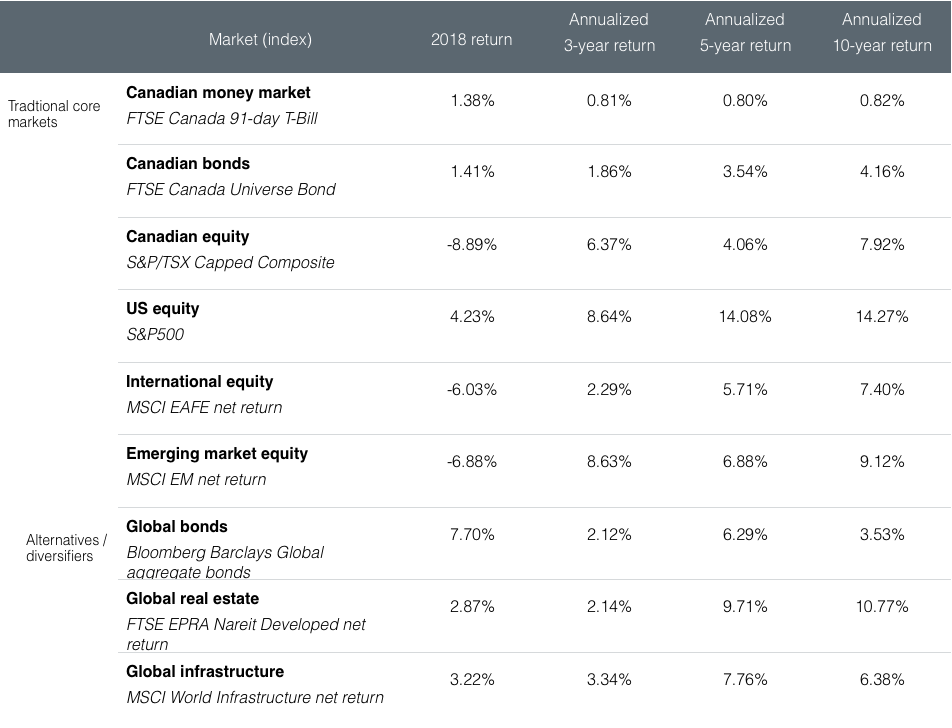

After a bull run that lasted 10 years, 2018 has seen most world equity markets finish with negative returns (expressed in Canadian dollars, except for the US market). However, global bonds and some alternative investments, such as global infrastructure and real estate, did offer a break, as did Canadian bonds, which generated slim positive returns. This makes for a good argument for diversification when investing.

The result is that a large portion of employees participating in Capital Accumulation Plans (CAPs), such as defined contribution pension plans, group Registered Retirement Savings Plans (RRSPs) or Deferred Profit Sharing Plans (DPSPs), will very likely see negative returns on their annual member statements for the first time. Employees may also be concerned by the level of market volatility experienced over the past year.

Market index returns on 31 December 2018 (in Canadian dollars)

Source: Morningstar Direct. Total returns gross of investment management and recordkeeping fees.

Target-date fund or lifecycle portfolio users

Most CAP participants now use ready-made investment portfolios, which automatically reduce exposure to risky assets as participants get closer to retirement. Due to the broad investment diversification these sophisticated solutions provide, they should somewhat limit the damage to member savings in company retirement plans.

Still, younger plan members will feel the heat in two ways: A large portion of their savings under this approach is invested in equity markets, and they likely have never experienced negative returns, so it may not be clear how they will react. Will they even notice?

Members getting closer to retirement are more likely to notice. Even though their equity exposure is much lower, bonds will have provided limited protection. As their accumulated savings should be much larger than their contributions, it is possible members will see a net decrease in their plan account balances compared to last year. Will this impact their retirement planning? Will they decide to continue working a bit longer?

Participants deciding on their own investments

Experience shows that members of all ages investing in a personalized, à la cartefashion (i.e., not using a ready-made approach, such as target date funds) tend to be more heavily invested in equities—particularly Canadian equities. Although this group should represent people who are more investment-savvy, that is not always the case, and some of these participants could be in for a bigger shock than expected.

Next steps

The 2018 situation is certainly not as dramatic as that of 2008, with its severe market crash. Even at that time, plan members had generally acted by doing nothing. Transactions in CAP accounts only slightly increased, meaning no panic movement happened. However, we still hear stories of employees nearing retirement having to postpone their departure date for a few years, or of others who questioned the oversight of the organization’s retirement plan. How will it play out this time, now that CAP accounts have grown significantly compared to 2008? It only takes a few nervous members to generate discussions about the company’s fiduciary responsibilities.

As the situation is not critical, we recommend employers keep an eye on plan members’ reactions, as they will shortly receive their annual account statements. Employers may then determine whether issuing a communication is the right thing to do. Reassuring members regarding the quality of the funds offered, providing them with a long-term view of capital markets and the company’s plan fund returns, reminding them of the benefits of diversification, and explaining the governance process in place are all things that should provide comfort and help members navigate these troubled waters.